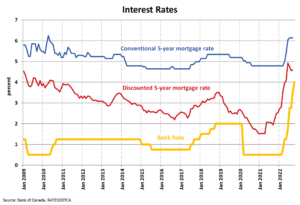

The Bank of Canada hiked its target for the overnight lending rate by 50 basis points to 3.75% while continuing its policy of quantitative tightening on Wednesday, October 26. Additionally, it was stated the policy rate could rise further given elevated inflation and inflation expectations as well as ongoing demand pressures in the economy.

Following the announcement, financial markets were pricing in at least another 25 to 50 basis points of further interest rate hikes through the third quarter of 2023.

The Bank acknowledged global inflation remains high and broad-based, reflecting the strength of the global recovery from the pandemic, supply chain disruptions, as well as elevated commodity prices stemming from the war in Ukraine. Financial stresses have started to increase in some economies as the strength of the U.S. dollar adds to inflationary pressures in many countries. Because of tighter global monetary policy, the Bank is expecting a sharp slowdown of the global economy in 2023.

The Bank noted the Canadian economy continues to operate in excess demand, and labour markets remain tight, with the demand for goods and services running ahead of the economy’s ability to supply them, which continues to put upward pressure on domestic inflation. Despite job vacancies declining from their peak, they remain high, and businesses continue to report widespread labour shortages. This, along with the excess demand created with the full reopening of the economy after pandemic restrictions, has led to large increases in the prices of both goods and services.

The Bank also highlighted higher interest rates are starting to have an effect in interest-sensitive areas of the economy including housing and spending on big-ticket items. The bank expects that “the contraction in residential investment that began in the second quarter of the year will continue through the first half of 2023,” and prices are “projected to continue to decline, particularly in those markets that saw larger increases during the pandemic.” Still, the Bank anticipates the effects of higher rates to take time to spread through the economy. With the pace of economic growth in Canada starting to slow, growth is projected to stall later this year and through the first half of 2023, declining from just over 3% in 2022 to just under 1% in 2023, with a modest increase of 2% expected in 2024.

While Consumer Price Index (CPI) inflation eased in September due to a drop in gasoline prices, it remains well above the Bank’s target range and has become more broad-based, with almost two-thirds of the components of CPI showing price increases of greater than 5% over the past year. Higher shelter costs and rising food prices are “stretching household budgets and creating hardship for many families in Canada.” As the economy responds to higher interest rates and elevated commodity prices and supply chain disruptions fade, inflation is expected to decline from around 7% in the fourth quarter of 2022 to around 3% in late 2023 and return to 2% by the end of 2024.

Canada’s major chartered banks are currently advertising five-year fixed mortgage special interest rates of around 5.54%. Home buyers can often negotiate the interest rate for mortgage financing based on their creditworthiness and the degree to which they do other banking business with the mortgage lender.

With the minimum qualifying rate for all mortgages being the greater of the mortgage contract rate +2% or 5.25% as set by the Office of the Superintendent of Financial Institutions (OSFI) and the Department of Finance, the stress-test hurdle in the fixed-rate and variable-rate space is now about 7.5% for new borrowers. All mortgage applicants must qualify for financing based on an interest rate no less than the benchmark five-year lending rate, even if the mortgage is for less than five years.

The Bank of Canada’s next scheduled interest rate announcement will be on December 7, 2022. The next full update of the Bank’s outlook for the economy and inflation, including risks to the projection, will be published in its Monetary Policy Report on January 25, 2023.

Source of Text: CREA (Canadian Real Estate Association)